Eventbrite has a new owner. Why organisers are reading the small print

Bending Spoons closed its $500m acquisition of Eventbrite in March 2026. What the buyer did at Evernote, Meetup, WeTransfer, Komoot and Vimeo, and what organisers should plan for.

On 10 March 2026, Eventbrite ceased to be a public company. The $500 million all-cash acquisition by Milan-based Bending Spoons, first announced in December 2025, closed earlier that week. Shareholders received $4.50 per share, the New York Stock Exchange delisted the stock, and Eventbrite became a wholly-owned subsidiary of one of Europe’s most active software acquirers.

For most of Eventbrite’s 4.7 million annual organisers, the transaction itself is a footnote. The relevant question is what happens next, and the most useful guide to that question is what Bending Spoons has done with the platforms it has already bought. The pattern is documented enough to draw on. It is also contested enough by Bending Spoons itself to be worth presenting with care.

What Bending Spoons does for a living

Bending Spoons describes itself as a long-term operator of digital products. In a rare extended interview with the Dutch investigative publication Follow the Money in late 2025, co-founder and CEO Luca Ferrari was explicit about the model: identify popular products with stagnant growth, buy them at a discount, hold them indefinitely, and operate them more profitably than their previous owners did.

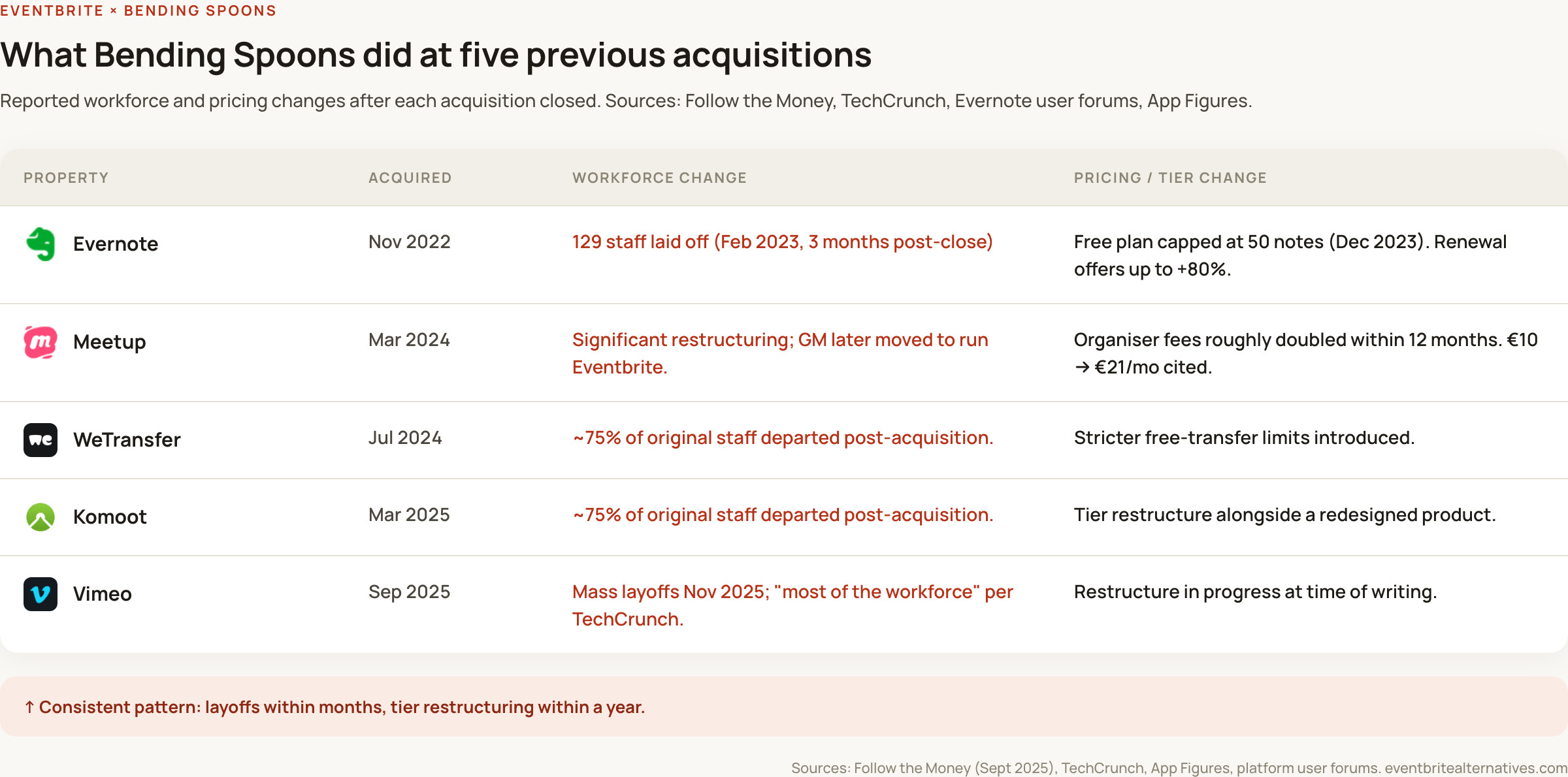

The portfolio bears this out. Since 2022, Bending Spoons has acquired Evernote, Meetup, WeTransfer, Komoot, Vimeo, StreamYard, Issuu, Brightcove and AOL, alongside Eventbrite. The combined group, according to its own disclosures, generates more than $2 billion in annual revenue and serves over 300 million monthly active users. The company was valued at $11 billion in a 2025 funding round.

What the company does after acquisition has settled into a recognisable shape across multiple deals. Three patterns appear consistently in the public record.

Significant workforce reductions. Within months of acquisition, headcount typically falls sharply. Bending Spoons laid off 129 Evernote staff in February 2023, three months after that deal closed. WeTransfer and Komoot both lost approximately 75% of their original staff post-acquisition, according to Follow the Money’s reporting. Vimeo experienced mass layoffs in late 2025 that, according to TechCrunch, hit “most of the workforce including the entire video team”. Bending Spoons attributes this to the consolidation of engineering, customer service and administration onto a single internal platform it calls a “universal OS”, which it argues allows acquired companies to operate with substantially less overhead.

Price and tier restructuring. Free tiers tend to tighten and paid tiers tend to rise. Evernote’s free plan, previously offering unlimited notes, was restricted to 50 notes per account in late 2023. The Evernote user forum recorded subscription renewal offers up to 80% higher than previous rates after Bending Spoons took ownership. WeTransfer added stricter limits on its free transfer service. Meetup organisers, according to multiple users interviewed by Follow the Money, saw their costs more than double, with one Dutch organiser citing a jump from below ten euros a month to twenty-one.

App Figures data, cited in Ticket Tailor’s analysis of the acquisition, shows a consistent revenue-up, usage-down pattern across Bending Spoons properties. That is the mathematical signature of higher prices applied to a shrinking but more lucrative user base.

Bending Spoons itself disputes the framing that this represents “alienating users”. In the Follow the Money interview, Ferrari pointed out that Meetup now has more non-paying organisers than paying ones, and that price increases for heavy users are typically paired with expanded free access for new ones. He also referenced product improvements across the portfolio, citing a hundred-item list of Evernote updates and a Komoot redesign that he said was developed in collaboration with experienced users. The company’s stated thesis is that previous ownership had under-invested in the products, that the post-acquisition restructure funds genuine improvement, and that the optics of layoffs and price rises obscure a longer-term value story.

Both readings exist in the evidence. What is harder to dispute is that the pattern is consistent enough across Evernote, WeTransfer, Meetup, Komoot and Vimeo that it now constitutes a track record, not a one-off.

Why Meetup is the closest parallel

Of the previous acquisitions, Meetup is the most directly comparable to Eventbrite. Both are event-discovery and organiser platforms built on network effects. Both depend on organisers continuing to use the platform to create the inventory of events that attracts attendees. Both have been around long enough to develop deeply embedded organiser bases who would find migration disruptive.

The two-year-old Meetup acquisition therefore represents the freshest data point on what Bending Spoons does with this specific category of product. The summary, as documented in multiple independent reports:

- Organiser fees roughly doubled within twelve months of the acquisition.

- The general manager brought in to run Meetup post-acquisition has now been appointed to run Eventbrite, according to industry trade press.

- Meetup’s organiser community has produced visible churn, with substantial Reddit and forum threads tracking organisers either leaving the platform or threatening to leave over feature paywalls and email deliverability issues.

- The product roadmap announced by Meetup’s leadership post-acquisition focused on backend reliability, organiser workflow improvements, and AI-driven recommendations, in roughly that order.

The Eventbrite roadmap announced post-acquisition has notable structural similarities. Bending Spoons’ stated focus areas include “improving reliability during key workflows”, making the platform “more intuitive and efficient from check-in to refunds and payouts”, and adding AI-assisted event creation, dedicated messaging, and a secondary ticket market. The product priorities are similar enough to Meetup’s that observers familiar with both have read it as evidence the same playbook is being applied.

None of this proves Eventbrite organisers will face fee increases. It does mean the question is now sufficiently live that any organiser using Eventbrite as critical operational infrastructure has a reasonable case to start planning for the possibility.

The financial reality of the deal

A few details of the transaction sharpen the analysis.

Bending Spoons paid approximately 1.7 times Eventbrite’s trailing twelve-month revenue of $295 million, well below typical SaaS valuations. The $500 million purchase price is itself a fraction of Eventbrite’s $1.76 billion valuation at its 2018 IPO. Annual revenue had been flat at around $325 million for the previous two fiscal years.

Bending Spoons financed the deal partly through a $2.8 billion debt round in 2025 led by Goldman Sachs and JP Morgan. The company’s overall leverage sits at roughly 2.7 times EBITDA, according to S&P. This is prudent for a portfolio with 50% margins, but it is leverage nonetheless, and leverage requires servicing. The capital structure creates a structural pressure to improve margins on acquired assets, which is precisely what the track record shows the company doing.

There is also a strategic dimension worth noting. Bending Spoons now owns both Eventbrite and Meetup, the two most recognisable event-discovery brands in the consumer internet. It also owns StreamYard, the live event production platform formerly part of Hopin. The shape of an events-and-content stack is visible in the portfolio, even if Bending Spoons has not yet articulated it as a strategic direction. Concentration of ownership at the top of a market typically does two things: it accumulates pricing power for the owner, and it expands the addressable market for alternatives operating below the consolidated layer.

What this looks like from an organiser’s perspective

The honest answer is that nobody outside Bending Spoons knows what will happen to Eventbrite’s fees, free tier, or feature set over the next twelve months. The company has indicated intentions to invest, and there is a reasonable case that the product will improve in ways that organisers will value, including AI-assisted event creation, better search and more reliable check-in flows.

There is an equally reasonable case, informed by the track record, that some combination of fee increases, tier restructuring, or feature paywalling will appear at some point in the next year or two. UK-based organisers have particular reason to pay attention to this, because Eventbrite already charges UK organisers a meaningfully higher rate (approximately 6.95% plus £0.59 per ticket) than its US baseline. Any increase compounds from a worse starting position.

Three groups of Eventbrite organisers seem most exposed to changes.

Organisers who rely on the free tier. Eventbrite reinstated unlimited free event publishing in 2024 as a founder-era move to re-stimulate organiser growth under public market pressure. That public-market pressure no longer exists. The free tier is an obvious lever for Bending Spoons to pull if it wants to improve margins, and the precedent at Evernote and WeTransfer is that free tiers have been the first to be restructured. Community organisers, charity fundraisers and free-event promoters have the strongest case to evaluate alternatives now rather than after a change is announced.

Mid-volume paid organisers. Organisers selling thousands of tickets a year on Eventbrite’s standard 3.7% + $1.79 per-ticket fee structure (US) or 6.95% + £0.59 (UK) are most exposed to any percentage-rate increase. A small change to a percentage fee scales rapidly across a year of events. These organisers also tend to have the most data-portability concerns, since their attendee lists, financial records and integrations may be deeply embedded in the platform.

Organisers using Eventbrite primarily for discovery. Eventbrite’s marketplace, with its 89 million monthly visitors, has been the platform’s strongest competitive advantage. Bending Spoons’ stated investment in search and AI-assisted discovery may strengthen this further. The trade-off, as it has been at Meetup, is whether marketplace value continues to justify the fee structure that funds it.

What’s already happening in the alternatives market

Industry trade publications and analysts have begun openly discussing the deal as a catalyst for movement in the self-service ticketing market. Event Tech Live, in coverage of the deal’s close, observed that “at least two platforms are actively recruiting Eventbrite organisers right now” and that “the alternatives are ready for your business”. TicketPeak, Humanitix, Ticket Tailor and TicketSource have all published analyses positioning themselves to organisers reconsidering Eventbrite.

Three points worth flagging about the alternatives landscape, regardless of which platform an organiser ultimately considers:

- 1. Most alternatives charge less than Eventbrite. TicketSpice’s $0.99 flat fee, Ticket Tailor’s from-$0.30 prepaid credits, Humanitix’s 2.1% + $0.99 (with charity discounts), and TicketSource’s bundled 7% all undercut Eventbrite’s effective rate on the typical event. Whether the saving is meaningful depends on volume and ticket price. Run your own numbers.

- 2. Marketplace discovery is the genuine trade-off. Most Eventbrite alternatives expect organisers to drive their own traffic rather than relying on platform-level discovery. For events targeting an existing audience, this is rarely a problem. For events that depend on people stumbling across them, it is.

- 3. Migration is easier now than it used to be. Most platforms support direct CSV imports, embedded ticketing on existing websites, and integration with Mailchimp or Stripe Connect for data continuity. The technical friction of switching is no longer the main barrier; the operational habit of using Eventbrite is.

The honest summary

The Bending Spoons acquisition does not automatically mean Eventbrite is about to become worse for organisers. It does mean the entity making decisions about Eventbrite’s fees, free tier, and feature gating has a documented history of restructuring those exact things at every other platform it has bought. The company itself disputes that this restructuring is harmful to users. The track record, the App Figures usage data, and the Meetup parallel suggest organisers should at least consider the question.

The most useful response to that uncertainty is probably the most boring one: do the work now. Calculate what you actually pay Eventbrite in a typical year. Identify which features you use and which platforms offer them. Test a small event on a shortlisted alternative before you need to migrate in a hurry. The cost of preparing for a change that might not come is a couple of hours. The cost of being unprepared if it does is measured in organiser revenue and operational disruption.

Eventbrite will publish its first significant product or pricing announcement under new ownership at some point in the coming months. That announcement will be the next real data point. Until then, the most defensible position for an organiser is to know what their alternatives look like, just in case.